Some time ago, I wrote about why I consider minimum wages unempowering and harmful to the least privileged members of society. I contended that minimum wages shut out from the labor market - a fundamental social institution - those people whose labor is least valuable. It prevents them from exercising what little power they have and perpetuates their disenfranchisement by preventing them from accumulating social and human capital through employment.

I'd like to revisit that topic briefly to better explain why a minimum wage effectively bars the least valuable, least privileged, and least powerful members of society from employment.

The process of establishing wages is effectively a negotiation between employer and employee. In some cases - when the employee's power is checked by the presence of many other potential employees - the employer can set the wage. In other cases - when the employer's power is checked by the presence of many other potential employers - the employee can set the wage. The freer the market, the less power both employee and employer have. All the rest of the time, employee and employer negotiate and arrive at a compromise.

Negotiations end when either the parties reach an agreement, or when one party walks away from the negotiation. The threat of walking away without a deal is a bargaining tactic.

This illuminates the brutal consequences of a minimum wage. In the presence of a minimum wage, the employer cannot offer a wage low enough to make the potential employee a contributing laborer. So the employer walks away from negotiation, leaving the employee out in the cold. The minimum wage effectively bars the least valued members of society from participating in the labor market not by outright exercise of force, but by the conjunction of freedom to walk away from negotiation and conditions on the price of labor.

In a modern, wealthy welfare state, the people most affected by the minimum wage and shut out from labor force participation move from job to job, work for cash, consume very little, and rely on friends, family, charity, and welfare. They're not starving to death, but they are shut out of permanent participation in the labor force. Thus they have difficulty accumulating social and human capital - they're stuck in an effective poverty trap.

So here are two general classes of solutions to this disenfranchisement. One type of solution is to remove the ability of employers to step away from the negotiating table. Mandate that employers take any job applicant and pay them a set wage.

The other type of solution - the type I favor: do away with the minimum wage and replace it with an anti-poverty measure that genuinely empowers the underprivileged, instead of one that merely looks nice to us upper-middle-class folks while silently disenfranchising the poorest, least valuable members of our society.

Tuesday, November 27, 2012

Saturday, November 17, 2012

332 straight months of above-average temperatures

I ran across this on Facebook today. It turns out that I have never, in my whole life, experienced a month with below-average temperatures:

This got me thinking about just what the chances of that are. I want to make one simple assumption and then test the hypothesis that global warming is not occurring.

Temperature Deviations

Let's look at temperature deviations. Call the average temperature over the century \(T\). We should think of this as the long-haul temperature. If global warming isn't happening, then this is the "baseline temperature" of the Earth.

Each month, the average temperature doesn't necessarily need to be the same as the long-haul temperature. It might be above or below, depending on whether there's something like El Nino going on, or if the sun is extra-bright, and so on. Either the temperature in that month is above or below the long-run temperature\(T\). Whether or not the temperature is above or below -- one of those two outcomes -- is what we'll focus on.

Here's our one simplifying assumption. The probability of monthly temperature being above or below \(T\) in one month does not depend on whether it was above or below \(T\) in previous months.

This lets us treat monthly temperature as a Bernoulli process. This is a standard piece of finite mathematics which I'll proceed to explain.

Bernoulli Processes

(If you want to get to the meat, skip this section and go to the next one.)

A Bernoulli process is an experiment with the same two outcomes ("success" and "failure") and the same two probabilities (of success, of failure) repeated over and over again. The probabilities don't change from experiment to experiment.

The standard example of a Bernoulli process is flipping a coin over and over again. There are two outcomes each time (heads and tails), and each time the probabilities are the same (\(0.5\)) each).

The usual question in a Bernoulli process is, "What's the probability of getting this many successes in that many trials?" For example, we might ask, "what's the probability of getting \(2\) heads if we flip a coin \(3\) times?" Here's a quick explanation of where the answer comes from. It requires two "black box facts."

We did not specify the order of the heads. So, for example, the outcomes HHT, HTH, THH all qualify as "three heads." Each of these outcomes has the same probability: since the probabilities don't change from experiment to experiment, the experiments are independent. Black-box fact one: The probability of a string of independent outcomes is the product of each outcome's probability. That is, the probability of HHT is the probability of H times the probability of H times the probability of T.

Now to get the probability of two heads (instead of HHT, say) we just have to add up the probabilities of all the different ways we can have two heads in three flips. Each has the same probability, so we just need to multiply that probability by the number of different ways we can get two heads in three flips. Black-box fact two: the number of ways of choosing two of the three flips to be heads (order doesn't matter) is the number \(C(3,2) = 3\).

So the probability of flipping two heads in three tosses is \(3(0.5)^3\).

More generally, the probability of getting \(k\) successes in \(n\) trials (if \(p\) is the probability of success and \(q\) is the probability of failure) is

$$C(n,k)p^kq^{n-k}.$$

Climate as Bernoulli Process

Our climate model is basically a series of coin flips. If the long-haul temperature average isn't changing, then each month, the probability of above-average temperatures is just the same as the probability of below-average temperatures. That is, there's a \(50\%\) chance that either occurs. We want to know the probability of \(332\) above-average temperatures in as many trials.

This just like treating each month as a coin flip. If you flip a coin \(332\) times, what's the chance that you get \(332\) heads in a row?

$$C(332,332)\bigg(\frac{1}{2}\bigg)^{332}\bigg(\frac{1}{2}\bigg)^0 = \frac{1}{2^{332}}.$$

That is an incredibly small, tiny, vanishing, eensy-weensy, little number. It's on the order of \(10^{-100}\), that is, one in \(10^{100}\). By comparison, there are roughly \(10^{80}\) atoms in the observable universe. So if we gathered all of those atoms into one box, colored one blue and all the rest white, and grabbed one of the atoms while blindfolded, we're billions of times more likely to pick the blue atom than we are to have \(332\) straight months of above-average temperatures.

The tl;dr? If global warming is not happening, and if the temperature each month is independent of the temperature the previous month, then the probability of \(332\) straight positive deviations is a billion trillion times less likely than reaching into a bin of all the atoms in the observable universe and randomly picking the one blue atom. So, global warming is almost certainly happening.

The average temperature across land and ocean surfaces during October was 14.63°C (58.23°F). This is 0.63°C (1.13°F) above the 20th century average and ties with 2008 as the fifth warmest October on record. The record warmest October occurred in 2003 and the record coldest October occurred in 1912. This is the 332nd consecutive month with an above-average temperature.In other words, for 332 straight months, the average temperature has been above the 20th century average temperature.

This got me thinking about just what the chances of that are. I want to make one simple assumption and then test the hypothesis that global warming is not occurring.

Temperature Deviations

Let's look at temperature deviations. Call the average temperature over the century \(T\). We should think of this as the long-haul temperature. If global warming isn't happening, then this is the "baseline temperature" of the Earth.

Each month, the average temperature doesn't necessarily need to be the same as the long-haul temperature. It might be above or below, depending on whether there's something like El Nino going on, or if the sun is extra-bright, and so on. Either the temperature in that month is above or below the long-run temperature\(T\). Whether or not the temperature is above or below -- one of those two outcomes -- is what we'll focus on.

Here's our one simplifying assumption. The probability of monthly temperature being above or below \(T\) in one month does not depend on whether it was above or below \(T\) in previous months.

This lets us treat monthly temperature as a Bernoulli process. This is a standard piece of finite mathematics which I'll proceed to explain.

Bernoulli Processes

(If you want to get to the meat, skip this section and go to the next one.)

A Bernoulli process is an experiment with the same two outcomes ("success" and "failure") and the same two probabilities (of success, of failure) repeated over and over again. The probabilities don't change from experiment to experiment.

The standard example of a Bernoulli process is flipping a coin over and over again. There are two outcomes each time (heads and tails), and each time the probabilities are the same (\(0.5\)) each).

The usual question in a Bernoulli process is, "What's the probability of getting this many successes in that many trials?" For example, we might ask, "what's the probability of getting \(2\) heads if we flip a coin \(3\) times?" Here's a quick explanation of where the answer comes from. It requires two "black box facts."

We did not specify the order of the heads. So, for example, the outcomes HHT, HTH, THH all qualify as "three heads." Each of these outcomes has the same probability: since the probabilities don't change from experiment to experiment, the experiments are independent. Black-box fact one: The probability of a string of independent outcomes is the product of each outcome's probability. That is, the probability of HHT is the probability of H times the probability of H times the probability of T.

Now to get the probability of two heads (instead of HHT, say) we just have to add up the probabilities of all the different ways we can have two heads in three flips. Each has the same probability, so we just need to multiply that probability by the number of different ways we can get two heads in three flips. Black-box fact two: the number of ways of choosing two of the three flips to be heads (order doesn't matter) is the number \(C(3,2) = 3\).

So the probability of flipping two heads in three tosses is \(3(0.5)^3\).

More generally, the probability of getting \(k\) successes in \(n\) trials (if \(p\) is the probability of success and \(q\) is the probability of failure) is

$$C(n,k)p^kq^{n-k}.$$

Climate as Bernoulli Process

Our climate model is basically a series of coin flips. If the long-haul temperature average isn't changing, then each month, the probability of above-average temperatures is just the same as the probability of below-average temperatures. That is, there's a \(50\%\) chance that either occurs. We want to know the probability of \(332\) above-average temperatures in as many trials.

This just like treating each month as a coin flip. If you flip a coin \(332\) times, what's the chance that you get \(332\) heads in a row?

$$C(332,332)\bigg(\frac{1}{2}\bigg)^{332}\bigg(\frac{1}{2}\bigg)^0 = \frac{1}{2^{332}}.$$

That is an incredibly small, tiny, vanishing, eensy-weensy, little number. It's on the order of \(10^{-100}\), that is, one in \(10^{100}\). By comparison, there are roughly \(10^{80}\) atoms in the observable universe. So if we gathered all of those atoms into one box, colored one blue and all the rest white, and grabbed one of the atoms while blindfolded, we're billions of times more likely to pick the blue atom than we are to have \(332\) straight months of above-average temperatures.

The tl;dr? If global warming is not happening, and if the temperature each month is independent of the temperature the previous month, then the probability of \(332\) straight positive deviations is a billion trillion times less likely than reaching into a bin of all the atoms in the observable universe and randomly picking the one blue atom. So, global warming is almost certainly happening.

Tuesday, November 13, 2012

Libertarianism as collectivism

I want to make an odd sort of point here. Usually, one thinks of libertarianism as an ideology focused on freedom and "collectivism" as describing an ideology which focuses on restraining freedom for the common good. I want to compare the two and troll around for interesting similarities.

Without being so pedantic as to pull up the dictionary definition, let's identify libertarianism as an ideology of government that holds the following: The best government enforces simple rules of property ownership and contract obligations and restrains coercive behavior (i.e., threat of force to extract negotiating concessions), but does not otherwise constrain behavior. Individual people should be (this ideology holds) free to move about and engage with each other in voluntary interactions.

Libertarian litererary works focus on freedom of action and contrast it with restrictions: Capitalism and Freedom, The Road to Serfdom, Free to Choose, Atlas Shrugged, and so on. The greatest good is achieved when the use of force is restricted to stopping the use of force.

Whence justification for this position? Libertarians are highly suspicious of centralized economic and social coordination for several reasons. These are perhaps the three most cited, aside from a moral imperative that freedom be preserved.

These justifications continue to claim that the well-being of society is higher with minimal government intervention. Libertarianism is a superior ideology, then, for utilitarian reasons: Society as a whole is better off with less central intervention, even if some people are worse off. The better-off people are better off than the worse-off people are worse off.

Collectivism is often thrown around as an epithet by libertarians: "Oh, you're a collectivist." (Apparently, it's often leveled at less dogmatic libertarians as well as at progressives, socialists, or communists --- in one entertaining account, Ludwig von Mises stormed out of a meeting of the Mont Pelerin Society after accusing Milton Friedman of being a socialist.) An ideology may be described as collectivist insofar as it requires the subordination of individual freedom and well-being to the collective good of all of society.

So here's the interesting comparison. Let's grant for a moment the proposal of utilitarian libertarians that a libertarian society is better off than a non-libertarian society. In particular, those who are less well-off than under alternative systems should accept that, for the greater good. Laid-off steel worker? Find a different job - your sacrifice enables lower prices for most people; they are better off than you are worse off. Trained as a vacuum-tube computer punch-card operator? Sorry, obsolete technology - we're all better off using semiconductor computers, except maybe you. Low education? Accept that minimum wage job - you're not capable of offering any more to society, and the resource use in a higher wage is better used elsewhere. If you don't like your circumstances, you should work to improve yourself, not expect society to dump resources into your life so you can be a net drain on it.

What is this, but collectivism? This vision of libertarianism sees humans like ants, and economic order in human society arising as spontaneously as order in an ant colony. To distort that spontaneous order is to hurt the colony as a whole; to embrace that spontaneous order is to embrace the greater good of the colony.

Meanwhile, no ant is intrinsically worthwhile. All ants contribute, and together create great things; but if an ant ceases to be a net contributor, it must change or cease to exist. Same with humans - as a professor of mine once indignantly exclaimed, "Why shouldn't people have to pay the costs they impose on other people?" (Corollary: If someone can't pay, why should they be able to exist?)

It seems to me that this libertarian perspective holds that, sometimes, in service to the greater good of society, people's livelihoods and well-being have to be sacrificed. Society is best off when resources are directed according to free markets, and if that hurts people - so be it; they must have been net drains on society. Thus: libertarianism as collectivism.

Without being so pedantic as to pull up the dictionary definition, let's identify libertarianism as an ideology of government that holds the following: The best government enforces simple rules of property ownership and contract obligations and restrains coercive behavior (i.e., threat of force to extract negotiating concessions), but does not otherwise constrain behavior. Individual people should be (this ideology holds) free to move about and engage with each other in voluntary interactions.

Libertarian litererary works focus on freedom of action and contrast it with restrictions: Capitalism and Freedom, The Road to Serfdom, Free to Choose, Atlas Shrugged, and so on. The greatest good is achieved when the use of force is restricted to stopping the use of force.

Whence justification for this position? Libertarians are highly suspicious of centralized economic and social coordination for several reasons. These are perhaps the three most cited, aside from a moral imperative that freedom be preserved.

- The Hayekian information problem: no single agent can have enough information to successfully coordinate economic activity.

- The public choice criticism: Dominant groups subvert central coordination to perpetuate their own dominance.

- The efficiency critique: A central planner will require the use of resources to centrally plan, and one large enough to direct the economy will consume a portion of economic resources that could be otherwise used for investment or consumption.

These justifications continue to claim that the well-being of society is higher with minimal government intervention. Libertarianism is a superior ideology, then, for utilitarian reasons: Society as a whole is better off with less central intervention, even if some people are worse off. The better-off people are better off than the worse-off people are worse off.

Collectivism is often thrown around as an epithet by libertarians: "Oh, you're a collectivist." (Apparently, it's often leveled at less dogmatic libertarians as well as at progressives, socialists, or communists --- in one entertaining account, Ludwig von Mises stormed out of a meeting of the Mont Pelerin Society after accusing Milton Friedman of being a socialist.) An ideology may be described as collectivist insofar as it requires the subordination of individual freedom and well-being to the collective good of all of society.

So here's the interesting comparison. Let's grant for a moment the proposal of utilitarian libertarians that a libertarian society is better off than a non-libertarian society. In particular, those who are less well-off than under alternative systems should accept that, for the greater good. Laid-off steel worker? Find a different job - your sacrifice enables lower prices for most people; they are better off than you are worse off. Trained as a vacuum-tube computer punch-card operator? Sorry, obsolete technology - we're all better off using semiconductor computers, except maybe you. Low education? Accept that minimum wage job - you're not capable of offering any more to society, and the resource use in a higher wage is better used elsewhere. If you don't like your circumstances, you should work to improve yourself, not expect society to dump resources into your life so you can be a net drain on it.

What is this, but collectivism? This vision of libertarianism sees humans like ants, and economic order in human society arising as spontaneously as order in an ant colony. To distort that spontaneous order is to hurt the colony as a whole; to embrace that spontaneous order is to embrace the greater good of the colony.

Meanwhile, no ant is intrinsically worthwhile. All ants contribute, and together create great things; but if an ant ceases to be a net contributor, it must change or cease to exist. Same with humans - as a professor of mine once indignantly exclaimed, "Why shouldn't people have to pay the costs they impose on other people?" (Corollary: If someone can't pay, why should they be able to exist?)

It seems to me that this libertarian perspective holds that, sometimes, in service to the greater good of society, people's livelihoods and well-being have to be sacrificed. Society is best off when resources are directed according to free markets, and if that hurts people - so be it; they must have been net drains on society. Thus: libertarianism as collectivism.

Friday, November 9, 2012

Is Indiana atypical?

Indiana consistently votes Republican. It was a MAJOR surprise to everyone involved when Indiana barely went for Obama in 2008. This is not typical of the Midwest: for the last twenty years, in successful Democratic election years, Indiana sticks up out of the South like a sore red thumb. (When a Republican takes the White House, Ohio often keeps Indiana company. While Ohio is a swing state, though, Republicans can count on Indiana for its solid dozen-or-so electoral votes.)

Short question: Is this atypical? The question was prompted by this amusing picture:

So I compared Indiana to its close neighbor Illinois, using the New York Times' data on each state. Glancing at county-by-county results, we see broadly similar trends: mostly red, with urban areas and some traditionally Democratic counties blue. The glaring source of difference between Illinois and Indiana is Chicago. I crunched a few numbers (rounding to the nearest thousand and ignoring third-party candidates - those will account for discrepancies of a few percentage points).

Illinois has 20 electoral votes, and just over 5 million votes (5,006,000) were cast in the state. Just under 2 million (1,918,000) of them were cast in Cook County. Obama carried Illinois with 57% of the vote, 2,916,000 votes, while Romney received 43%, or 20,990,000 votes.

Indiana, meanwhile, has 11 electoral votes. In Indiana, 2,552,000 votes were cast, with 1,412,000 (or 54%) cast for Romney and 1,140,000 (44%) cast for Obama.

Let's suppose that Cook County just suddenly fell into Lake Michigan. What would happen to Illinois' vote totals? Well, instead of 5 million votes, only a handful more than 3 million votes would be cast (much closer to Indiana's 2.6 million total). Removing the Cook County voting from the Obama-Romney statewide totals gives Romney 1,611,000 votes to Obama's 1,477,000 votes. This is an edge of 52% - 48% to Romney (much closer to Indiana's 55%-45%). Romney would get Illinois' electoral votes ... but there wouldn't be 20 anymore. Crude scaling suggests there would be 12 electoral votes (hey, Indiana has 11!).

Neat, huh? If Illinois didn't have Chicago, it would function like Indiana's twin: A state with a couple of mid-sized, moderately dense cities (Indianapolis, Fort Wayne, Evansville, South Bend, ...) in a sea of rural conservative counties. A huge, dense urban area makes the difference between a reliable large Democratic state and a reliable mid-sized Republican state.

What about Ohio, Indiana's other neighbor? It doesn't have any one tremendously huge, dense urban area, nor does it have only a few - instead, it has several large, dense cities spread throughout the state (Cincinnati, Cleveland, Toledo, Columbus, Dayton, Youngstown). The urban/rural tension is finely balanced, so Ohio functions as a swing state.

Thursday, August 23, 2012

Problematicity of minimum wages

We can express a minimum wage as a price floor in each labor market. Simple models indicate that minimum wages have no effect in high-wage markets and cause unemployment in low-wage markets; the overall effect on unemployment should be relatively low, since the median hourly wage is roughly $16.50.

I don't want to discuss the empirics of the minimum wage here; we'll save that for a future post. Many arguments about the minimum wage focus on its reduction of quantity of labor demanded, or increase of quantity of labor supplied. Some focus on unemployment. Others focus on the infringement of contractual freedom (a perpetual, and to me perplexing, obsession of libertarians).

Rather than use those arguments, I'll argue from a moral perspective: Imposing a minimum wage marginalizes those whose labor is less valuable than the minimum wage indicates and robs them of autonomy and dignity. This imposition disproportionately affects underprivileged groups, since their lack of privilege translates into labor of lower value. If we wish to assist underprivileged and marginalized groups, we should find a way to do so that supports their autonomy and dignity, rather than effectively punishing them for having time worth less than the minimum wage.

Pecuniary value exists entirely in the eye of the beholder; an asset is only and precisely as valuable as what others are willing to exchange for it. I shall refer to pecuniary value as "value." Market process discovers the pecuniary value of assets and, over time, matches assets to those who place the highest value on them.

One important observation is that value can only be discovered. It cannot be declared. One cannot declare, "This home is worth $300,000!" and cause the home to be worth $300,000 --- the home's value can only be ascertained by the bids of those who are interested in purchasing.

We may regard time as an asset: one exchanges time (in the form of giving up alternative uses to perform certain obligations) for money. The wage rate, reflects the value of one's time. If people are willing to pay me $35 for an hour of instruction, then an hour of my time is worth at least $35. (I paper over the distinction between marginal value and value.)

The labor market is an emergent social mechanism involving suppliers of labor and buyers of labor. It acts to discover the value of each worker's time and match that worker to the employer who values her time most highly. Each transaction is an approximate lower bound on the value of the time of the worker.

Imposing a floor on the price of labor declares that no employer may purchase time worth less than this bound. Those whose time is worth less than the bound are shut out from participating in the labor market. (In practice, they may participate, but will not be formally hired - hence the increase in unemployment. Or they will participate in informal labor arrangements.)

The minimum wage declares: If your labor is worth less than this wage, you are excluded. You may not participate in this fundamental social institution. Effectively, a minimum wage sets a minimum worthy value to time and outlaws the employment of people whose time is worth less than that minimum worthy value --- it marginalizes individuals with time less valuable than the wage.

This marginalization disproportionately impacts underprivileged groups, whose time is often worth less because of this underprivileging. Because current employment -- by generating experience and connections, for example -- usually increases the future value of labor, effective minimum wages perpetuate the impoverishment and disenfranchisement of those groups.

In addition to blocking a mechanism that can act to correct social injustice, a minimum wage robs autonomy and dignity from those whose time is worth less than the minimum wage. Instead of seeking the greatest value for their time, people with time worth less than the minimum wage are forced to either endure a perpetual, humiliating series of rejections, or to operate outside the law, or to simply withdraw from a fundamental social institution. In our society, participation in the labor market confers a measure of dignity; to eject a person from the labor market, to bar him from participation, is to strip him of dignity.

Perhaps minimum wages are instituted as a mere signal of group affiliation, or in a misguided attempt to help underprivileged groups, rather than as a mechanism to perpetuate social inequity and drive underprivileged groups outside the confines of the law. In any case, the moral impact of a minimum wage is to strip of dignity those it affects. It serves to create outlaws and reinforces existing structures of oppression.

If we truly wish to help underprivileged groups whose labor is worth little, we should do so in a way that preserves their dignity and autonomy and does not drive them outside of the law in search of betterment. We should do so in a way that respects basic, unquestionable human rights to shelter and sustenance without depriving already-impoverished people of more opportunities to participate in society and better themselves.

Edit 3:20 pm, 8/23:

A friend points out that in some cases --- where markets do not nearly approximate free --- there may be a power differential that acts in wage negotiations. In this case, a minimum wage law not only shuts out those with labor worth the least, but those who have the least power. Instead of permitting them to exercise what little power they can, it simply removes them from the process. We create the illusion of empowerment, when in reality those who have the least power are simply barred from participation.

If we wish to empower the least privileged, most marginalized, we need a system of social insurance that actually empowers them, rather than shutting them out of a fundamentally dignifying social process. A minimum wage removes options and strips dignity; a healthy social insurance system would give additional options, truly empowering the least privileged people in our society, giving them dignity and autonomy.

I don't want to discuss the empirics of the minimum wage here; we'll save that for a future post. Many arguments about the minimum wage focus on its reduction of quantity of labor demanded, or increase of quantity of labor supplied. Some focus on unemployment. Others focus on the infringement of contractual freedom (a perpetual, and to me perplexing, obsession of libertarians).

Rather than use those arguments, I'll argue from a moral perspective: Imposing a minimum wage marginalizes those whose labor is less valuable than the minimum wage indicates and robs them of autonomy and dignity. This imposition disproportionately affects underprivileged groups, since their lack of privilege translates into labor of lower value. If we wish to assist underprivileged and marginalized groups, we should find a way to do so that supports their autonomy and dignity, rather than effectively punishing them for having time worth less than the minimum wage.

Pecuniary value exists entirely in the eye of the beholder; an asset is only and precisely as valuable as what others are willing to exchange for it. I shall refer to pecuniary value as "value." Market process discovers the pecuniary value of assets and, over time, matches assets to those who place the highest value on them.

One important observation is that value can only be discovered. It cannot be declared. One cannot declare, "This home is worth $300,000!" and cause the home to be worth $300,000 --- the home's value can only be ascertained by the bids of those who are interested in purchasing.

We may regard time as an asset: one exchanges time (in the form of giving up alternative uses to perform certain obligations) for money. The wage rate, reflects the value of one's time. If people are willing to pay me $35 for an hour of instruction, then an hour of my time is worth at least $35. (I paper over the distinction between marginal value and value.)

The labor market is an emergent social mechanism involving suppliers of labor and buyers of labor. It acts to discover the value of each worker's time and match that worker to the employer who values her time most highly. Each transaction is an approximate lower bound on the value of the time of the worker.

Imposing a floor on the price of labor declares that no employer may purchase time worth less than this bound. Those whose time is worth less than the bound are shut out from participating in the labor market. (In practice, they may participate, but will not be formally hired - hence the increase in unemployment. Or they will participate in informal labor arrangements.)

The minimum wage declares: If your labor is worth less than this wage, you are excluded. You may not participate in this fundamental social institution. Effectively, a minimum wage sets a minimum worthy value to time and outlaws the employment of people whose time is worth less than that minimum worthy value --- it marginalizes individuals with time less valuable than the wage.

This marginalization disproportionately impacts underprivileged groups, whose time is often worth less because of this underprivileging. Because current employment -- by generating experience and connections, for example -- usually increases the future value of labor, effective minimum wages perpetuate the impoverishment and disenfranchisement of those groups.

In addition to blocking a mechanism that can act to correct social injustice, a minimum wage robs autonomy and dignity from those whose time is worth less than the minimum wage. Instead of seeking the greatest value for their time, people with time worth less than the minimum wage are forced to either endure a perpetual, humiliating series of rejections, or to operate outside the law, or to simply withdraw from a fundamental social institution. In our society, participation in the labor market confers a measure of dignity; to eject a person from the labor market, to bar him from participation, is to strip him of dignity.

Perhaps minimum wages are instituted as a mere signal of group affiliation, or in a misguided attempt to help underprivileged groups, rather than as a mechanism to perpetuate social inequity and drive underprivileged groups outside the confines of the law. In any case, the moral impact of a minimum wage is to strip of dignity those it affects. It serves to create outlaws and reinforces existing structures of oppression.

If we truly wish to help underprivileged groups whose labor is worth little, we should do so in a way that preserves their dignity and autonomy and does not drive them outside of the law in search of betterment. We should do so in a way that respects basic, unquestionable human rights to shelter and sustenance without depriving already-impoverished people of more opportunities to participate in society and better themselves.

Edit 3:20 pm, 8/23:

A friend points out that in some cases --- where markets do not nearly approximate free --- there may be a power differential that acts in wage negotiations. In this case, a minimum wage law not only shuts out those with labor worth the least, but those who have the least power. Instead of permitting them to exercise what little power they can, it simply removes them from the process. We create the illusion of empowerment, when in reality those who have the least power are simply barred from participation.

If we wish to empower the least privileged, most marginalized, we need a system of social insurance that actually empowers them, rather than shutting them out of a fundamentally dignifying social process. A minimum wage removes options and strips dignity; a healthy social insurance system would give additional options, truly empowering the least privileged people in our society, giving them dignity and autonomy.

Sunday, August 19, 2012

Privilege informs misunderstanding of "consent"

Here at my university, we have posters up here and there indicating what "consent" means. If she's too drunk to talk, asleep, unconscious, or does anything except explicitly indicate "yes," then sex is actually rape.

Why? Because in a sexually charged, intimate situation, miscommunication is very easy. If expectations are mismatched, or if there's a slight difference in body language interpretation, miscommunication can cause heady fun to disorientingly transform into violation. Better to be a little awkward at first than to risk inadvertently hurting your partner.

Here's a simple story based on sexual dimorphism that predicts miscommunication. Men are bigger and stronger (on average) than women. A woman who is making out with a larger man she does not know extremely well is making risk assessments for the (low-probability, but very high-cost) case that the encounter becomes violent and balancing those against the (high-probability, high-benefit) case the encounter remains pleasant.

So let us suppose the woman does not give consent to sex. If the man continues to press for sex, the woman's assessment that probability that the encounter becomes violent rises.* One (common?) strategy is to continue to withhold verbal consent, but to grudgingly, unenthusiastically go along with intercourse, in order to avoid potential violence. This is being raped, and it's probably a much more common type of rape than stereotypical home invasions or abductions.

From the man's perspective, it looks exactly like he has simply convinced her to change her mind, except she's just less enthusiastic than she was before. He is making no threat assessments, so he judges her to not be making any either. She goes along with it; he would not go along with sex if he didn't want to have sex, so he judges that she is consenting. If she intended the "no" to be permanent, she would have reinforced "no" when he pressed -- that's what he would have done -- so he judges the lack of reinforcement as evidence that she has implicitly consented.

This is exactly what she intends! Causing him to believe she is consenting, even if she does not consent, removes the possibility that he violently assaults her. She is engaged in sex against her wishes, but has minimized harm.

Observe here that "male privilege" --- the man's perspective does not take into account the calculation the woman has to make concerning him --- leads to misinterpretation of behavior, and hence of the nature of consent. Whereas the behavior actually communicates, "I'll do it because I don't want you to assault me," the man evaluates it to mean, "I changed my mind to 'yes.'"

* You lose all the futures where he says "Okay!" and goes back to making out.

Why? Because in a sexually charged, intimate situation, miscommunication is very easy. If expectations are mismatched, or if there's a slight difference in body language interpretation, miscommunication can cause heady fun to disorientingly transform into violation. Better to be a little awkward at first than to risk inadvertently hurting your partner.

Here's a simple story based on sexual dimorphism that predicts miscommunication. Men are bigger and stronger (on average) than women. A woman who is making out with a larger man she does not know extremely well is making risk assessments for the (low-probability, but very high-cost) case that the encounter becomes violent and balancing those against the (high-probability, high-benefit) case the encounter remains pleasant.

So let us suppose the woman does not give consent to sex. If the man continues to press for sex, the woman's assessment that probability that the encounter becomes violent rises.* One (common?) strategy is to continue to withhold verbal consent, but to grudgingly, unenthusiastically go along with intercourse, in order to avoid potential violence. This is being raped, and it's probably a much more common type of rape than stereotypical home invasions or abductions.

From the man's perspective, it looks exactly like he has simply convinced her to change her mind, except she's just less enthusiastic than she was before. He is making no threat assessments, so he judges her to not be making any either. She goes along with it; he would not go along with sex if he didn't want to have sex, so he judges that she is consenting. If she intended the "no" to be permanent, she would have reinforced "no" when he pressed -- that's what he would have done -- so he judges the lack of reinforcement as evidence that she has implicitly consented.

This is exactly what she intends! Causing him to believe she is consenting, even if she does not consent, removes the possibility that he violently assaults her. She is engaged in sex against her wishes, but has minimized harm.

Observe here that "male privilege" --- the man's perspective does not take into account the calculation the woman has to make concerning him --- leads to misinterpretation of behavior, and hence of the nature of consent. Whereas the behavior actually communicates, "I'll do it because I don't want you to assault me," the man evaluates it to mean, "I changed my mind to 'yes.'"

* You lose all the futures where he says "Okay!" and goes back to making out.

Thursday, August 16, 2012

A Song of Sticky Wages (Told in Pictures)

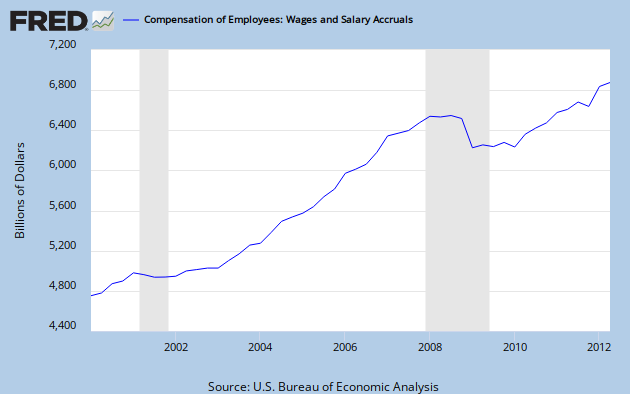

During the recession, total income contracted:

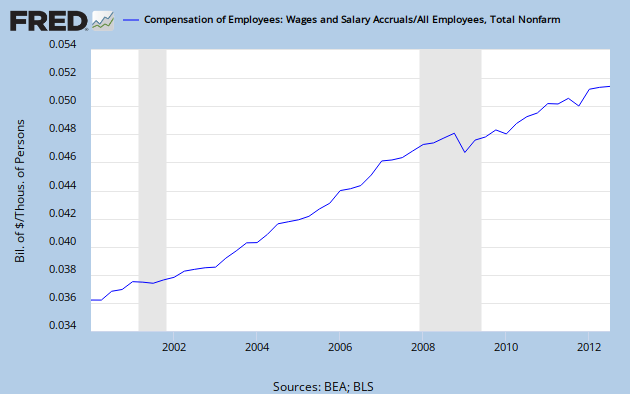

Income from total employee wages also fell significantly:

Income from total employee wages also fell significantly:

(This is the sum of all wages and salaries paid to everyone in the country. It's the single largest component of income. I'll call it "total wages.")

(This is the sum of all wages and salaries paid to everyone in the country. It's the single largest component of income. I'll call it "total wages.")

Why did total wages fall? Let's add another line, total number of (nonfarm, seasonally adjusted) employees:

Unemployment has been persistently high. Why? Wages have continued to grow a little bit more slowly than total wages, and total wages are locked in as a fraction of total income. Thus:

Wages are at a level that produced full employment in 2007, but total income, and hence total wages, are far below that level. The difference is made up in the misery of 5,000,000 people.

Let's examine more closely the relationship between a persistent shortfall in income and unemployment. Let's look at the ratio of actual income to potential income. Here's are the two graphs, one since 2000 and one since 1949. Look at how closely unemployment tracks the income gap:

We should hypothesize that, because of sticky wages, there is a strong positive correlation between this ratio (which I'll call income shortfall or NGDP shortfall) and unemployment. Surprise!

(Data are quarterly, 1949Q1-2012Q2.)

If we look more recently, 2000-2012, we see the same pattern:

In this case, it's tighter because over a mere decade we shouldn't see a large shift in the natural rate of unemployment.

So we see that a sharp shock to income down to a new trend is what causes persistent high unemployment. As Scott Sumner memorably analogized:

Why did total wages fall? Let's add another line, total number of (nonfarm, seasonally adjusted) employees:

Care: the scale of the red line is on the right hand side. Total wages fell because income fell. Let's verify this by looking at wages per person, what I'll call "wages," computed by dividing total wages and total employment. What happened?

Wages stagnated but did not fall. In other words, wage growth dropped to zero and then the rest of the total wage drop manifested in layoffs. After the recession was over, wages per person picked up right where they left off and continued growing, albeit at a slightly lower rate.

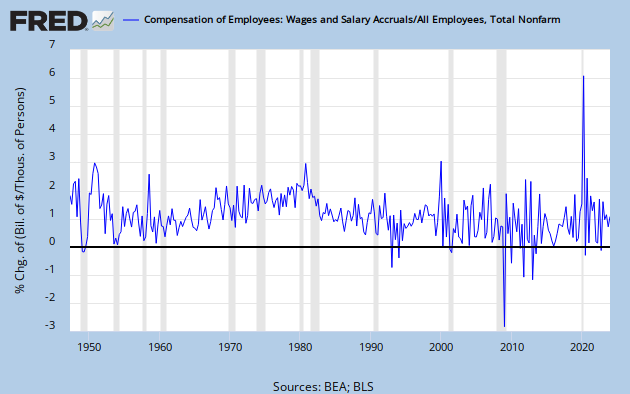

This looks to be a general phenomenon. Here's the whole time series of per-employee wages, from 1939 to 2012, presented as quarter-on-quarter percentage change. Observe that it has dropped below zero precisely four quarters in the last 80 years - and each time it promptly bounced back up. Even during recessions, wage growth keeps rising. These are called "sticky wages."

So what happens in a bad recession? Total income falls and wages fall in proportion. That wage drop manifests itself in a drop in per-employee wage growth to zero, and thereafter people are simply laid off. After the recession is over, wages resume their upward trend.

Let's look at it like this. Total wages are some (more or less fixed) fraction of total income -- roughly half. In a recession, total income falls, so total wages have to fall as well. First, wages stop growing. Then, since wages don't fall and thus don't keep pace with the fall in total wages, people start getting laid off.

Let's now look at the source of the drop in total wages. Wages fell because income fell: observe that the ratio of total wages to income (green line, right scale) stayed roughly constant over the course of the 2008 recession. Total wages and income are red and blue, respectively, and measured on the left scale.

(As an aside, this constancy was actually a stay in a secular decline; most of the rest of income goes to capital, and income inequality fell drastically during the recession.)

Note that after the fall in incomes, they did not rise back to their initial trend. We can measure potential income, which is what the economy could be producing if it were at full employment, and compare it to actual income:

Unemployment has been persistently high. Why? Wages have continued to grow a little bit more slowly than total wages, and total wages are locked in as a fraction of total income. Thus:

Wages are at a level that produced full employment in 2007, but total income, and hence total wages, are far below that level. The difference is made up in the misery of 5,000,000 people.

Let's examine more closely the relationship between a persistent shortfall in income and unemployment. Let's look at the ratio of actual income to potential income. Here's are the two graphs, one since 2000 and one since 1949. Look at how closely unemployment tracks the income gap:

We should hypothesize that, because of sticky wages, there is a strong positive correlation between this ratio (which I'll call income shortfall or NGDP shortfall) and unemployment. Surprise!

(Data are quarterly, 1949Q1-2012Q2.)

If we look more recently, 2000-2012, we see the same pattern:

In this case, it's tighter because over a mere decade we shouldn't see a large shift in the natural rate of unemployment.

So we see that a sharp shock to income down to a new trend is what causes persistent high unemployment. As Scott Sumner memorably analogized:

NGDP shocks are like a game of musical chairs. Remove 9% of NGDP relative to trend, and you'll have 9,000,000 unemployed workers sitting on the floor. It's that simple.

Wages will slowly adjust downwards (since total wage growth has been greater than wage growth) and labor market hysteresis will reduce the workforce. The former is incorporated in the new income trend, and the both pull potential income down to the new income trend. The economy will return to full employment. But at what cost?

Addendum: There may be some concern that the correlation between income shortfall and unemployment is artificial - that is, that potential income is computed using the unemployment rate, so I'm merely expressing a tautology. For further reading, here is the CBO's explanation of their method for computing potential income.

Wednesday, August 15, 2012

Privilege - what is it?

So I've been thinking about what "privilege" is and how to apply recognition of the idea in everyday life. A personal project of mine is trying to translate ideas from humanities into forms that make intuitive sense to me, giving them precise definitions. Maybe these thoughts will be useful to other people as well.

Here's a simple definition from Finally Feminism 101:

(Side note: It is also interesting to remove society from the definition and make another definition:

This may not be a good more general definition because it conflates with an identical use: "X privilege" means, I think, "advantage conferred to group X over group not-X by the configuration of society with respect to X." For instance, "male privilege" is advantage conferred to men over women by the configuration of society with respect to men; white privilege is advantage conferred to white people over non-white people by the configuration of society with respect to race; etc.)

"Privilege" is an empirical claim. It can be supported or disproven by observation. For instance, "men have privilege in the workforce" makes the prediction that men should have, all else equal, higher salaries. They do. So this is evidence for the proposition that society's configuration gives men an advantage in the workplace.

Privilege is a statement about groups, so it only extends stochastically to individuals. Nonetheless, since individuals make decisions based on limited information and assessments of probabilities, this stochastic extension impacts individual behavior. (Interesting implication: The perception of privilege can create privilege where none actually existed.)

Since basic human instinct is to evaluate others' situations by placing ourselves into their spots, privilege can be difficult to detect for members of the privileged group. Because of the advantage conferred by privilege, a member of the privileged group performing simple first-order analysis on the motivations and behavior of a member of the non-privileged group will fail to detect factors for which the non-privileged person must account in optimizing well-being. (More on this below.)

Privilege could be "intrinsic," in the sense that one group in society possesses a set of values or characteristics that give it an advantage over other groups. For instance, suppose that upper-middle class families have a culture that emphasizes education and long-term investment in human capital, while lower class families do not. Given a broader society that is configured to reward education and long-term investment over short-term consumption, we could say that this is an example of upper-middle class privilege over lower classes. (If this is not an example of privilege, then the definition needs to be modified to exclude this case and others like it.)

Not all privilege is good; not all privilege is bad. Some groups are privileged in some areas and underprivileged in other areas. (For example, mathematicians are privileged, apparently, in precise logical thinking, but underprivileged in social subtleties. Victorian upper-class women were privileged in their treatment by men, but severely underprivileged in freedom.) Given a group, one can probably measure all the privilege it has and all the underprivileges it has and judge whether it is net positive or negative.

In practice, what does this mean? While I was following a little bit of that Rebecca-Watson-got-creeped-on-in-an-elevator story (I refuse to call it "elevatorgate" because appending "-gate" to the end of every salacious outburst is just ridiculous -- it was the name of the hotel, people), I realized this: recognizing privilege is just modifying the golden rule.

We all know the golden rule. We learn it in preschool, taking our first steps into a larger world of social interaction. "Do to others what you want them to do to you." We tell it to our children: "Kiddo, would you like it if he hit you? Then don't hit him." It has arisen in religious and philosophical teaching independently across the world.

Why is it useful? As humans, we all have some basic beliefs in common - we want social interactions to be pleasant, we don't want to get hit, we don't want to have our stuff taken, so on. Internalizing the golden rule amounts to recognizing this commonality: we can predict other people's reactions to our behavior by placing ourselves on the opposite ends of our interaction.

But as we pass on to interaction with broader and more diverse people, our approach needs to become a little more sophisticated. Here's a motivating example. Until last spring, there was an abandoned building about a block away from our apartment. It was between us and our jobs. I hadn't really noticed it before, but my wife drew my attention to it: she wanted me to walk her home from her job. Why? Because of that abandoned building.

It would never have occurred to me to be creeped out by the building. When I put myself in her place -- which wasn't hard, because I had walked past it many times! -- I still wasn't creeped out walking past it. It was only when I modified my analysis of her motivations to take into account differences between us that I understood why she felt the building was creepy.

She's weaker than I am and can't run as fast. Her chances of being the target of an assault are much higher than mine. (They're still statistically small, given our class and neighborhood, and even smaller, but still high enough, with bad enough consequences that she needs to take them into account). So, in the exact same situation, she is rationally more cautious than I am.

To recognize privilege (if it exists), you have to modify the golden rule. When you're evaluating someone else's motivations and behavior, you have to ask yourself not just "what would I do in his circumstance?" but "how is he different from me and how does that difference impact what I'd do in his circumstance?"

A privilege is an advantage enjoyed by one group over another that is bestowed by the current configuration of society (and not by, say, biology or geography). Privilege between individuals is stochastically inherited from groups, and manifests itself in differences in evaluation of the same situation. It can be detected by modifying the golden rule from "Put yourself in their shoes" to "Put yourself in their shoes, then ask how they're different from you and how that difference would impact your response."

Definition

Here's a simple definition from Finally Feminism 101:

Privilege is an advantage conferred by the configuration of society to some groups over other groups.What do we mean here by advantages? Let us say that an "advantage of X over Y" is a benefit X enjoys in reaching X's goals that Y does not enjoy in reaching Y's goals. So, unwinding, privilege of some group over another means that the way society is configured gives the first group benefits in reaching their goals that the second group does not receive in reaching their goals.

(Side note: It is also interesting to remove society from the definition and make another definition:

X privilege is an advantage conferred by configuration of X to some groups over other groups.So, "social privilege" would be a class of advantages conferred by the configuration of society. Meanwhile, "biological privilege" would be a class of advantages conferred by the configuration of biology to some groups over others --- for instance, men are biologically privileged with strength and not-having-babies, people without disabilities are biologically privileged over people with disabilities, and so on.

This may not be a good more general definition because it conflates with an identical use: "X privilege" means, I think, "advantage conferred to group X over group not-X by the configuration of society with respect to X." For instance, "male privilege" is advantage conferred to men over women by the configuration of society with respect to men; white privilege is advantage conferred to white people over non-white people by the configuration of society with respect to race; etc.)

Some observations.

"Privilege" is an empirical claim. It can be supported or disproven by observation. For instance, "men have privilege in the workforce" makes the prediction that men should have, all else equal, higher salaries. They do. So this is evidence for the proposition that society's configuration gives men an advantage in the workplace.

Privilege is a statement about groups, so it only extends stochastically to individuals. Nonetheless, since individuals make decisions based on limited information and assessments of probabilities, this stochastic extension impacts individual behavior. (Interesting implication: The perception of privilege can create privilege where none actually existed.)

Since basic human instinct is to evaluate others' situations by placing ourselves into their spots, privilege can be difficult to detect for members of the privileged group. Because of the advantage conferred by privilege, a member of the privileged group performing simple first-order analysis on the motivations and behavior of a member of the non-privileged group will fail to detect factors for which the non-privileged person must account in optimizing well-being. (More on this below.)

Privilege could be "intrinsic," in the sense that one group in society possesses a set of values or characteristics that give it an advantage over other groups. For instance, suppose that upper-middle class families have a culture that emphasizes education and long-term investment in human capital, while lower class families do not. Given a broader society that is configured to reward education and long-term investment over short-term consumption, we could say that this is an example of upper-middle class privilege over lower classes. (If this is not an example of privilege, then the definition needs to be modified to exclude this case and others like it.)

Not all privilege is good; not all privilege is bad. Some groups are privileged in some areas and underprivileged in other areas. (For example, mathematicians are privileged, apparently, in precise logical thinking, but underprivileged in social subtleties. Victorian upper-class women were privileged in their treatment by men, but severely underprivileged in freedom.) Given a group, one can probably measure all the privilege it has and all the underprivileges it has and judge whether it is net positive or negative.

Application

In practice, what does this mean? While I was following a little bit of that Rebecca-Watson-got-creeped-on-in-an-elevator story (I refuse to call it "elevatorgate" because appending "-gate" to the end of every salacious outburst is just ridiculous -- it was the name of the hotel, people), I realized this: recognizing privilege is just modifying the golden rule.

We all know the golden rule. We learn it in preschool, taking our first steps into a larger world of social interaction. "Do to others what you want them to do to you." We tell it to our children: "Kiddo, would you like it if he hit you? Then don't hit him." It has arisen in religious and philosophical teaching independently across the world.

Why is it useful? As humans, we all have some basic beliefs in common - we want social interactions to be pleasant, we don't want to get hit, we don't want to have our stuff taken, so on. Internalizing the golden rule amounts to recognizing this commonality: we can predict other people's reactions to our behavior by placing ourselves on the opposite ends of our interaction.

But as we pass on to interaction with broader and more diverse people, our approach needs to become a little more sophisticated. Here's a motivating example. Until last spring, there was an abandoned building about a block away from our apartment. It was between us and our jobs. I hadn't really noticed it before, but my wife drew my attention to it: she wanted me to walk her home from her job. Why? Because of that abandoned building.

It would never have occurred to me to be creeped out by the building. When I put myself in her place -- which wasn't hard, because I had walked past it many times! -- I still wasn't creeped out walking past it. It was only when I modified my analysis of her motivations to take into account differences between us that I understood why she felt the building was creepy.

She's weaker than I am and can't run as fast. Her chances of being the target of an assault are much higher than mine. (They're still statistically small, given our class and neighborhood, and even smaller, but still high enough, with bad enough consequences that she needs to take them into account). So, in the exact same situation, she is rationally more cautious than I am.

To recognize privilege (if it exists), you have to modify the golden rule. When you're evaluating someone else's motivations and behavior, you have to ask yourself not just "what would I do in his circumstance?" but "how is he different from me and how does that difference impact what I'd do in his circumstance?"

Conclusion

A privilege is an advantage enjoyed by one group over another that is bestowed by the current configuration of society (and not by, say, biology or geography). Privilege between individuals is stochastically inherited from groups, and manifests itself in differences in evaluation of the same situation. It can be detected by modifying the golden rule from "Put yourself in their shoes" to "Put yourself in their shoes, then ask how they're different from you and how that difference would impact your response."

Tuesday, August 14, 2012

Where does understanding math break down?

I received my fall teaching assignment this week. Next Monday, I stand up in front of 80 or so nervous students who have to pass this class in order to graduate, and I start telling them about math they've probably never seen before.

Most of them already have mental blocks in place telling them that math is difficult. Many of them struggled in their high school math classes as they moved from arithmetic to algebra and geometry. Instead of introspecting to figure out what they were doing wrong, they decided it was too "difficult" for them. So they enter my class with trepidation, and they're already setting themselves up to fail it.

To facilitate learning, one of my tasks is to convince my students that they actually can learn math, that it's not too difficult. In fact, I contend that the sort of math I'm teaching is, in principle, not difficult at all. That's what I want to ruminate about in this post.

In this type of math class, we have three basic threads interacting. First, we have definitions: I write down symbols, I tell you what they mean, I tell you why they mean this, and I give you some simple examples. Second, we have techniques: I tell you how and why in this class of situations, we use these symbols, and in that class of situations, we use those symbols. Third, we have problems: I give you a problem, you figure out which class of situations it falls in, and then you use the symbols and their meaning to tell me something about the problem.

Let me give you an example.

The definition. A binomial coefficient is this symbol: for any two positive integers \(n\) and \(k\) with \(n > k\),

\[ C(n,k) = \frac{n!}{k!(n-k)!}.\]

Here \(n! = n(n-1)(n-2)\cdots 3\cdot 2\cdot 1\), the product of all the numbers from \(1\) to \(n\). In fact, we can write down

\[C(n,k) = \frac{n(n-1)(n-2)\cdots(n-k+1)}{k(k-1)(k-2)\cdots 3\cdot 2\cdot 1}.\]

That is, we take \(k\) slots, start with \(n\) and continue on down, multiplying as we go, then divide that product by \(k!\).

What it means. A binomial coefficient tells you how many unordered combinations of \(k\) things you can draw from \(n\) things. That is, it is the number of \(k\)-element subsets in an \(n\)-element set. This is because the number of ways of picking \(k\) things in order is counted by \(\frac{n!}{k!}\) and the number of ways of ordering those \(k\) things is \(k!\), so to see how many ways there are of picking \(k\) things without regard to order, we divide the number of total ways of picking \(k\) things in order by the number of ways of picking the same \(k\) things in different orders.

Example. To see this in action, check out

\[ C(5,3) = \frac{5\cdot 4\cdot 3}{3\cdot 2\cdot 1} = 10.\]

The general class of situations. You use a binomial coefficient any time you want to count the number of ways of choosing \(k\) things from \(n\) things without regard to order.

A particular example. Say you have five different sandwiches and you grab three of them. How many different outcomes does this experiment have? Well, since you're just grabbing them, you're obviously not making a point of checking what order you're taking them. So you're just choosing \(3\) things from \(5\) things without regard to order. How many ways are there of doing this? \(C(5,3) = 10.\)

Where could the process of understanding break down? You might have just skimmed this because you've already decided you won't ever understand math. If that's the case, I'd encourage you to go back and read it again. It's not as bad as you think it is.

Perhaps your eyes glossed over at the symbol \(C(n,k)\). If that's the case, remember: I told you what the symbol means. I don't expect you to remember it right away, because it's unfamiliar and new -- but remember that its definition is right there! Any time you need to remember it, you can just go back and double-check what it means.

Maybe you didn't quite catch why binomial coefficients count unordered combinations. If so, that's all right; that's a dense paragraph and in the interest of brevity (and accuracy - the whys get short shrift in the classroom) I left out some small steps. But if you read it a few times, I don't doubt that you'll come to understand.

(I recognize that if this is new to you, you won't catch all of it right away. I can do this off the top of my head because I've taught this material for several years. But if you take enough time to practice, you'll come to grasp the idea, just as if you shoot enough baskets, you'll be able to hit a free throw.)

So where else could a student's understanding break down? There's always the possibility that the student is blowing off the class (because they don't think they're able to do it?). I don't have too much control over that.

Perhaps students' understanding fails not for any single process, but when many new, related ideas are thrown at them very quickly. Part of learning mathematics is building up heuristics which indicate which tool to use in a given problem. If students do not focus sufficiently on distinguishing related ideas from each other, then their heuristics will confuse related but distinct situations and the intuition they develop will not conform to reality.

For example, related to the idea of binomial coefficients measuring unordered combinations is permutation coefficients measuring ordered combinations. The number of ways of drawing \(k\) items from \(n\) items, counted in order, is \(P(n,k) = \frac{n!}{(n-k)!} = n(n-1)(n-2)\cdots (n-k+1).\) One way we help students remember is, if there are \(k\) items, you draw \(k\) slots. There are \(n\) ways of filling the first slot, \(n-1\) ways of filling the second slot, and so on. Then you multiply them all together. This tool is used to count the number of ordered \(k\)-tuples that can be created from an \(n\)-element set.

If the problem is the same as above --- five sandwiches, you grab three --- a student might reason this way: There are three sandwiches, so I draw three slots. There are five ways of filling the first slot, four ways of filling the second slot, and three ways of filling the third slot, so there must be sixty ways of drawing three sandwiches from five sandwiches.

Where did the student's reasoning go wrong? Take a minute and figure it out.

The student's intuition is misshapen: He did not consider order. The student has internalized that, in any problem that involves drawing items from a larger set, the number of ways of drawing items can be found by drawing a slot for each item, then counting the number of items to be included in each slot.

In principle, (this kind of) math isn't difficult. It's no harder than learning a foreign language. You just have to remember the meanings of new symbols, how to use them, and which situations call for using those symbols. A computer could do it (and anything a computer can do is not difficult, just tedious).

Perhaps failing students just move too fast, gulping instead of chewing, so that their intuitions malfunction? Or they just don't put in the time and practice necessary for remembering these new, foreign symbols? Or is there some fundamental limitation that I just don't see?

Edit:

Addendum -- One friend asked me, "Where does 'binomial coefficient' come from?" A binomial is the sum of two algebraic terms: \(a + b\). If you take an integer power of a binomial, you get the following polynomial:

\[(a+b)^n = \sum_{k = 0}^n C(n,k)a^kb^{n-k}\]

\[ = a^n + na^{n-1}b + \frac{n(n-1)}{2}a^{n-2}b^2 + \cdots + \frac{n(n-1)(n-2)\cdots 3\cdot 2}{(n-2)(n-4)\cdots 3\cdot 2\cdot 1}a^2b^{n-2} + nab^{n-1} + b^n.\]

So the "binomial coefficients" are coefficients (numbers by which variable expressions are multiplied) in the polynomial you get by raising a binomial to a power.

Most of them already have mental blocks in place telling them that math is difficult. Many of them struggled in their high school math classes as they moved from arithmetic to algebra and geometry. Instead of introspecting to figure out what they were doing wrong, they decided it was too "difficult" for them. So they enter my class with trepidation, and they're already setting themselves up to fail it.

To facilitate learning, one of my tasks is to convince my students that they actually can learn math, that it's not too difficult. In fact, I contend that the sort of math I'm teaching is, in principle, not difficult at all. That's what I want to ruminate about in this post.

In this type of math class, we have three basic threads interacting. First, we have definitions: I write down symbols, I tell you what they mean, I tell you why they mean this, and I give you some simple examples. Second, we have techniques: I tell you how and why in this class of situations, we use these symbols, and in that class of situations, we use those symbols. Third, we have problems: I give you a problem, you figure out which class of situations it falls in, and then you use the symbols and their meaning to tell me something about the problem.

Let me give you an example.

The definition. A binomial coefficient is this symbol: for any two positive integers \(n\) and \(k\) with \(n > k\),

\[ C(n,k) = \frac{n!}{k!(n-k)!}.\]

Here \(n! = n(n-1)(n-2)\cdots 3\cdot 2\cdot 1\), the product of all the numbers from \(1\) to \(n\). In fact, we can write down

\[C(n,k) = \frac{n(n-1)(n-2)\cdots(n-k+1)}{k(k-1)(k-2)\cdots 3\cdot 2\cdot 1}.\]

That is, we take \(k\) slots, start with \(n\) and continue on down, multiplying as we go, then divide that product by \(k!\).

What it means. A binomial coefficient tells you how many unordered combinations of \(k\) things you can draw from \(n\) things. That is, it is the number of \(k\)-element subsets in an \(n\)-element set. This is because the number of ways of picking \(k\) things in order is counted by \(\frac{n!}{k!}\) and the number of ways of ordering those \(k\) things is \(k!\), so to see how many ways there are of picking \(k\) things without regard to order, we divide the number of total ways of picking \(k\) things in order by the number of ways of picking the same \(k\) things in different orders.

Example. To see this in action, check out

\[ C(5,3) = \frac{5\cdot 4\cdot 3}{3\cdot 2\cdot 1} = 10.\]

The general class of situations. You use a binomial coefficient any time you want to count the number of ways of choosing \(k\) things from \(n\) things without regard to order.

A particular example. Say you have five different sandwiches and you grab three of them. How many different outcomes does this experiment have? Well, since you're just grabbing them, you're obviously not making a point of checking what order you're taking them. So you're just choosing \(3\) things from \(5\) things without regard to order. How many ways are there of doing this? \(C(5,3) = 10.\)

Where could the process of understanding break down? You might have just skimmed this because you've already decided you won't ever understand math. If that's the case, I'd encourage you to go back and read it again. It's not as bad as you think it is.

Perhaps your eyes glossed over at the symbol \(C(n,k)\). If that's the case, remember: I told you what the symbol means. I don't expect you to remember it right away, because it's unfamiliar and new -- but remember that its definition is right there! Any time you need to remember it, you can just go back and double-check what it means.

Maybe you didn't quite catch why binomial coefficients count unordered combinations. If so, that's all right; that's a dense paragraph and in the interest of brevity (and accuracy - the whys get short shrift in the classroom) I left out some small steps. But if you read it a few times, I don't doubt that you'll come to understand.

(I recognize that if this is new to you, you won't catch all of it right away. I can do this off the top of my head because I've taught this material for several years. But if you take enough time to practice, you'll come to grasp the idea, just as if you shoot enough baskets, you'll be able to hit a free throw.)

So where else could a student's understanding break down? There's always the possibility that the student is blowing off the class (because they don't think they're able to do it?). I don't have too much control over that.

Perhaps students' understanding fails not for any single process, but when many new, related ideas are thrown at them very quickly. Part of learning mathematics is building up heuristics which indicate which tool to use in a given problem. If students do not focus sufficiently on distinguishing related ideas from each other, then their heuristics will confuse related but distinct situations and the intuition they develop will not conform to reality.

For example, related to the idea of binomial coefficients measuring unordered combinations is permutation coefficients measuring ordered combinations. The number of ways of drawing \(k\) items from \(n\) items, counted in order, is \(P(n,k) = \frac{n!}{(n-k)!} = n(n-1)(n-2)\cdots (n-k+1).\) One way we help students remember is, if there are \(k\) items, you draw \(k\) slots. There are \(n\) ways of filling the first slot, \(n-1\) ways of filling the second slot, and so on. Then you multiply them all together. This tool is used to count the number of ordered \(k\)-tuples that can be created from an \(n\)-element set.

If the problem is the same as above --- five sandwiches, you grab three --- a student might reason this way: There are three sandwiches, so I draw three slots. There are five ways of filling the first slot, four ways of filling the second slot, and three ways of filling the third slot, so there must be sixty ways of drawing three sandwiches from five sandwiches.

Where did the student's reasoning go wrong? Take a minute and figure it out.

The student's intuition is misshapen: He did not consider order. The student has internalized that, in any problem that involves drawing items from a larger set, the number of ways of drawing items can be found by drawing a slot for each item, then counting the number of items to be included in each slot.

In principle, (this kind of) math isn't difficult. It's no harder than learning a foreign language. You just have to remember the meanings of new symbols, how to use them, and which situations call for using those symbols. A computer could do it (and anything a computer can do is not difficult, just tedious).

Perhaps failing students just move too fast, gulping instead of chewing, so that their intuitions malfunction? Or they just don't put in the time and practice necessary for remembering these new, foreign symbols? Or is there some fundamental limitation that I just don't see?

Edit:

Addendum -- One friend asked me, "Where does 'binomial coefficient' come from?" A binomial is the sum of two algebraic terms: \(a + b\). If you take an integer power of a binomial, you get the following polynomial:

\[(a+b)^n = \sum_{k = 0}^n C(n,k)a^kb^{n-k}\]

\[ = a^n + na^{n-1}b + \frac{n(n-1)}{2}a^{n-2}b^2 + \cdots + \frac{n(n-1)(n-2)\cdots 3\cdot 2}{(n-2)(n-4)\cdots 3\cdot 2\cdot 1}a^2b^{n-2} + nab^{n-1} + b^n.\]

So the "binomial coefficients" are coefficients (numbers by which variable expressions are multiplied) in the polynomial you get by raising a binomial to a power.

Sanity from the Boston Fed

Eric Rosengren, president of the Boston Fed, interviewed by Jeremy Hobson on Marketplace. Here are some excerpts.

Whether the Fed should continue waiting and seeing:

Should policy actually be tied to results?

"You think that you can see a direct connection at some point between the Fed pumping money into the economy essentially, and somebody getting a job somewhere?"

What about inflation? (Probably a response to Dallas Fed president Fisher.)

Go listen to the entire interview. Hopefully, now that the July jobs report is in, the doves will push their case harder at the next meeting.

Whether the Fed should continue waiting and seeing:

My own expectation is that the second half of the year won't be much better than the first half, because the drivers of fiscal austerity and European problems aren't likely to be resolved in the next two quarters, and that monetary policy shouldn't wait any further before reacting to the global slowdown that we've been encountering.

Should policy actually be tied to results?